Cashback vs Miles: Which One Gives More Value in 2026?

Every time someone gets a credit card in Singapore, they eventually face the same question:

Should I chase cashback or miles?

Cashback sounds simple. You spend money, you get money back.

Miles sounds more exciting. You spend money, earn points, and eventually redeem them for flights, upgrades, or even business-class seats.

But in 2026, with higher living costs, rising travel demand, card restrictions, minimum spends, cashback caps, foreign currency fees, and miles devaluation risks, the better question is not:

“Which one gives more value?”

It is:

“Which one gives more value for the way I actually spend?”

Because the wrong card strategy can make you feel like you are “earning rewards” while actually leaving money on the table.

The Simple Difference Between Cashback and Miles

Cashback is straightforward. You receive a rebate, usually as a statement credit, cash credit, or rewards that reduce your card bill.

Miles are different. Instead of getting cash back directly, you earn points or miles that can be converted into airline miles and used for flights, upgrades, or travel perks.

MoneySmart’s 2026 guide summarises the difference clearly: cashback cards offer direct, predictable savings on daily spending such as groceries, dining, and transport, while miles cards are better suited to travellers who want flight perks, upgrades, and travel-related value.

So the first distinction is this:

Reward type

What you get

Main benefit

Cashback

Money back

Simple, predictable savings

Miles

Travel rewards

Potentially higher value, especially for premium flights

Cashback is easier to understand. Miles can be more powerful, but only if you know how to redeem them well.

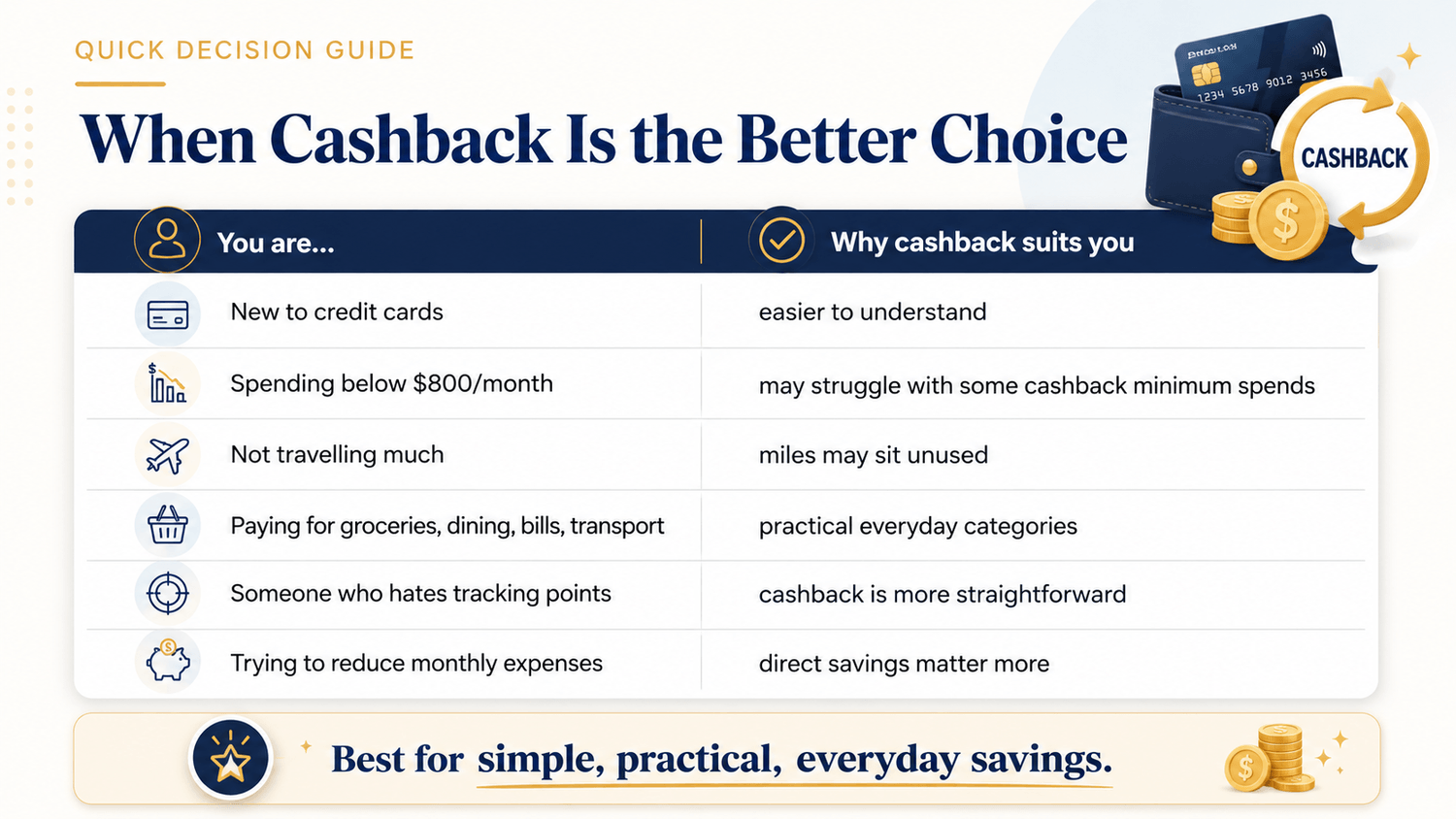

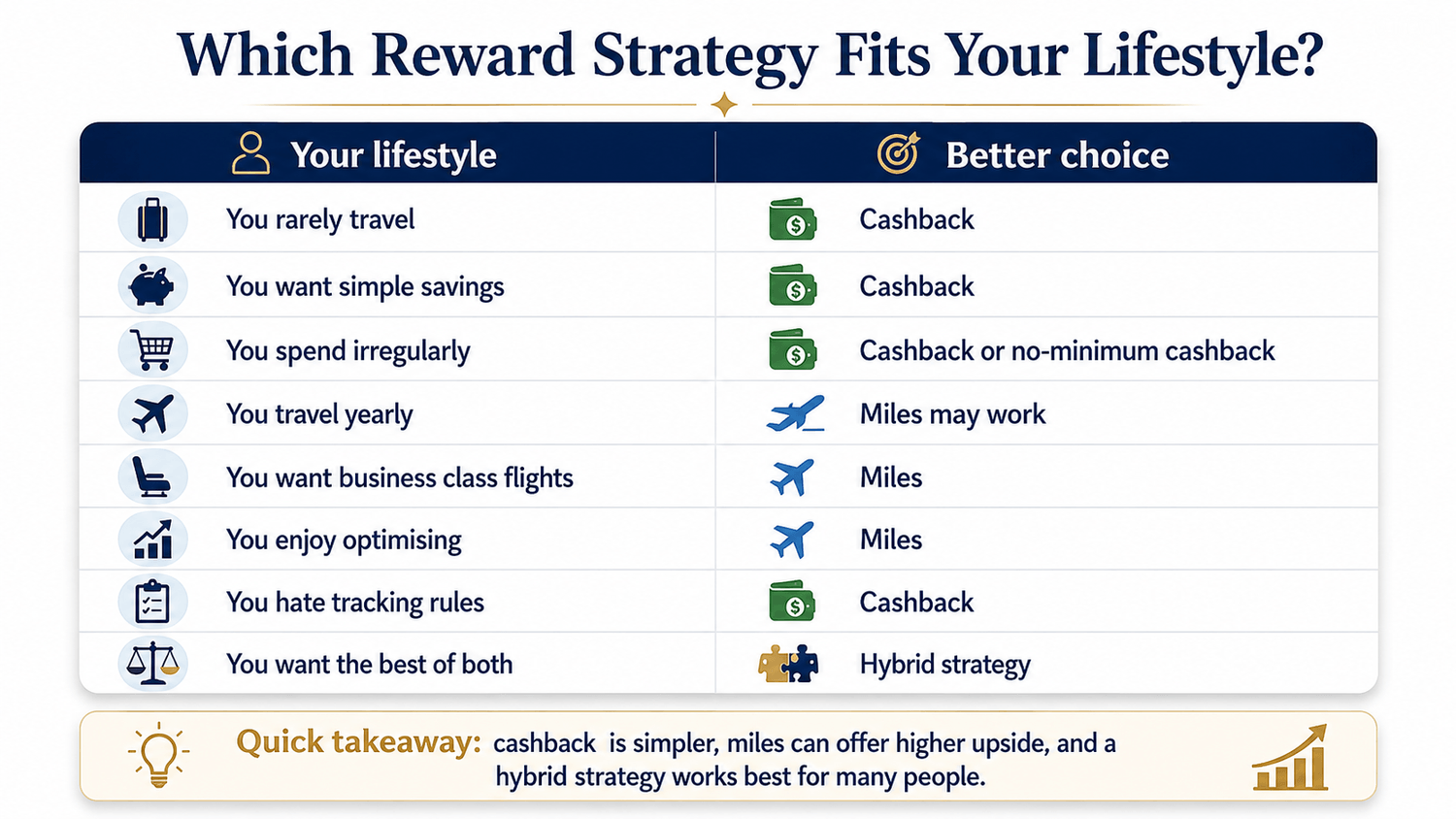

Why Cashback Feels Better for Most People

Cashback wins on simplicity. You do not need to understand award charts, redemption availability, transfer partners, fuel surcharges, blackout dates, or whether one mile is worth 1 cent or 2 cents. You just spend, meet the card conditions, and get a rebate.

That makes cashback especially attractive if your spending is mainly on:

Spending pattern

Why cashback may work better

Groceries

Predictable monthly spend

Dining

Easy category matching

Transport

Daily recurring expense

Online shopping

Often eligible for higher cashback categories

Bills

Practical everyday savings

Low-to-moderate spend

Easier to benefit without chasing large redemptions

MoneySmart’s cashback credit card guide says choosing the right cashback card is not just about the highest advertised rate, but about matching the card to your actual spending patterns, such as groceries, dining, commuting, or online shopping.

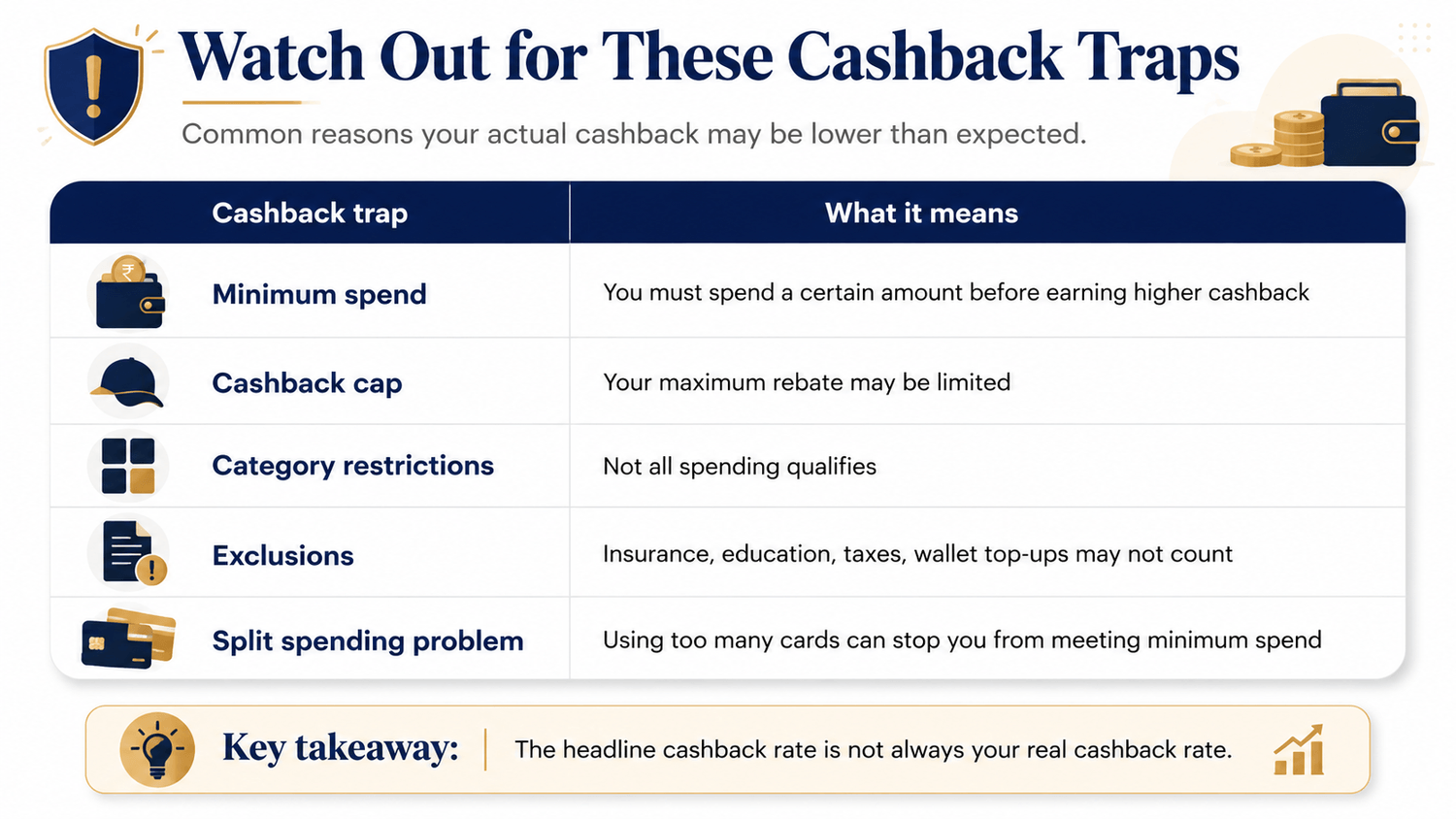

That is important because cashback cards often come with conditions. Some cards require a minimum monthly spend. Some cap the cashback you can earn. Some give high rates only on specific categories. SingSaver’s 2026 credit card strategy guide notes that many popular cashback cards have minimum spend thresholds around S$800 or S$1,000 per month, and if your spending is below that, a no-minimum-spend card may be more suitable. So cashback is simple, but not always effortless. The mistake people make is looking only at the headline rate.

For example:

“Up to 8% cashback” sounds amazing. But if the card has an $800 minimum spend, category exclusions, and a monthly cashback cap, your real return may be much lower.

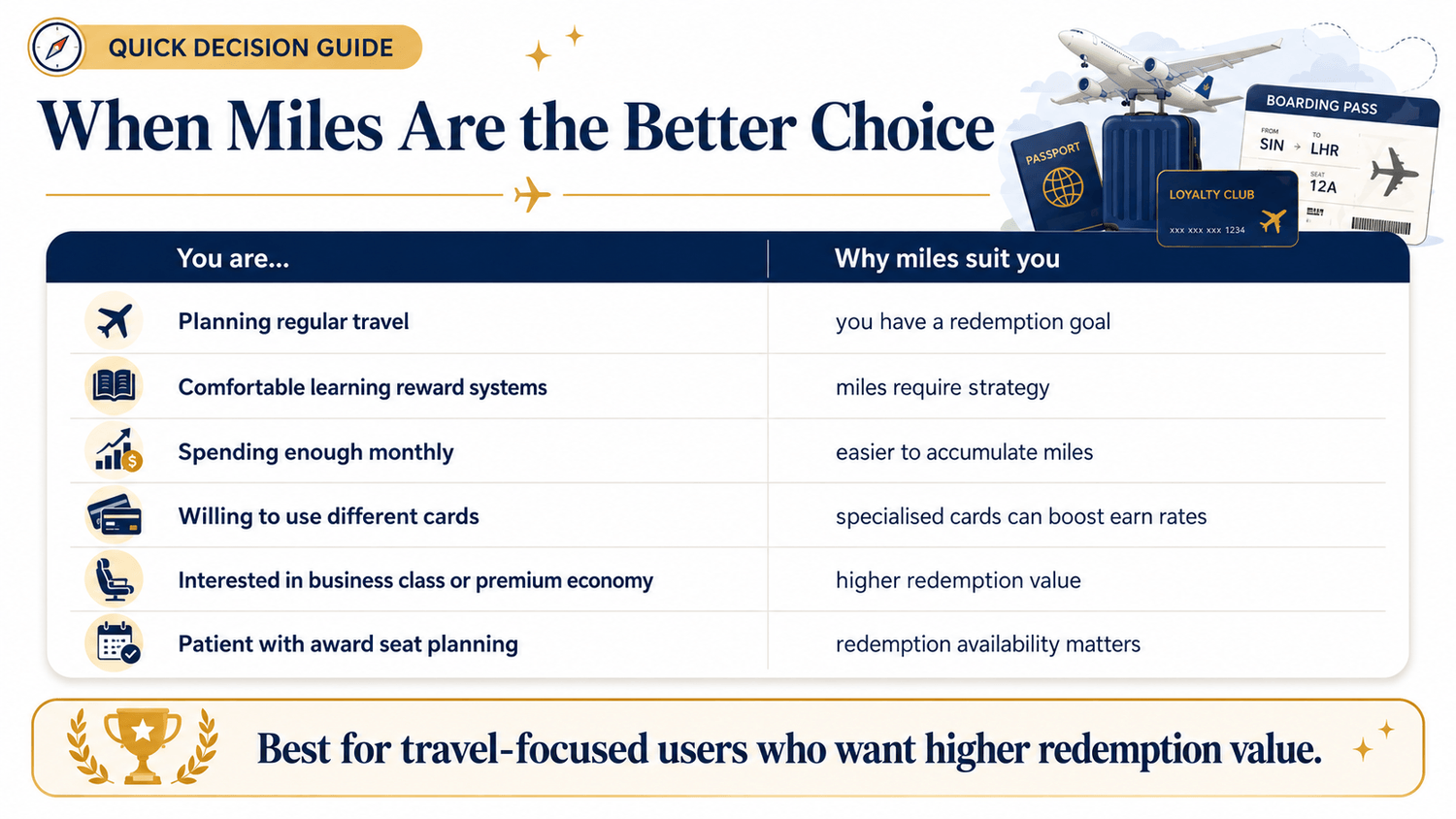

Why Miles Can Give More Value

Miles can be more valuable than cashback because travel redemptions are not always valued at a fixed cash rate. A cashback card that gives 1.5% back gives you $1.50 for every $100 spent.

A miles card earning 4 miles per dollar gives you 400 miles for every $100 spent. The value depends on how you redeem those miles. If you redeem miles poorly, the value may be mediocre. If you redeem miles well, especially for premium cabin flights, the value can beat cashback. ShopBack’s 2026 travel credit card guide says miles cards can outperform cashback cards for Singaporeans spending on flights and hotels if the miles are redeemed for business or premium economy travel, where a mile may be worth around SGD 0.015 to SGD 0.025. It also notes that cashback may be simpler if you usually fly economy and prefer cash in hand.

That is the real miles game.

Miles work better if you…

Why it matters

Travel at least once or twice a year

You have a real use for the miles

Can plan redemptions early

Award seats are limited

Redeem for long-haul or premium cabins

cents-per-mile value is higher

Spend enough to accumulate meaningful miles

Small miles balances can sit unused

Are okay with complexity

Miles require more tracking

Choosing between miles, cashback, or rewards depends on your spending habits and priorities.

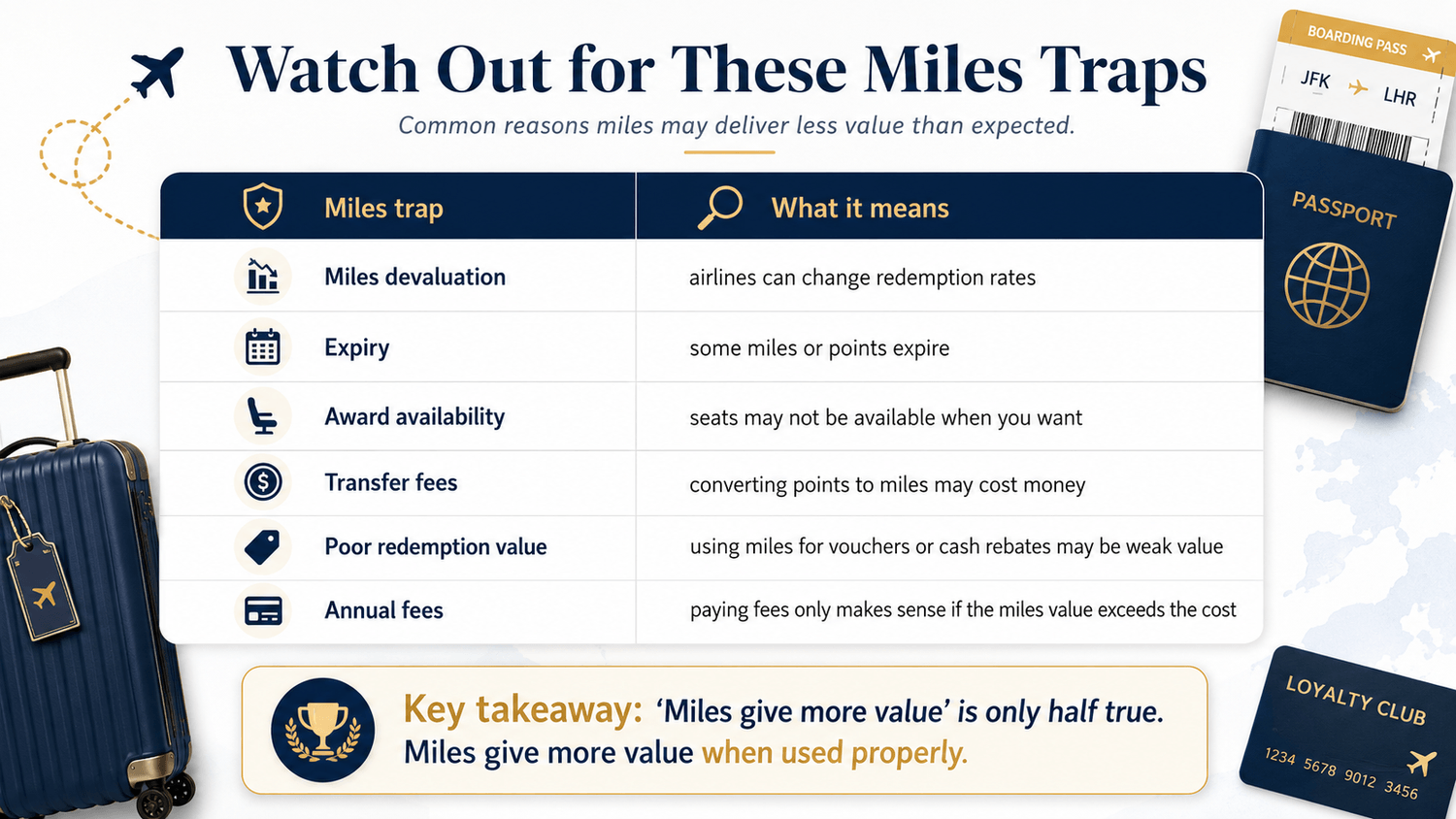

So miles are not “free travel.” They are a game of optimisation.

The Real Comparison: Guaranteed Value vs Potential Value

The best way to explain cashback vs miles is this:

Factor

Cashback

Miles

Value type

Guaranteed

Potential

Ease of use

Very easy

More complexe.

Best for

Everyday savings

Travel redemptions

Main risk

Caps and minimum spend

Poor redemption value

Emotional appeal

Practical

Aspirational

Best user

Consistent local spender

Frequent or strategic traveller

Cashback gives you less drama. Miles gives you more upside. But the upside only matters if you actually use it.

Example: Spending $2,000 a Month

Let’s say you spend $2,000 a month, or $24,000 a year, on eligible credit card spend.

Cashback scenario

If your average cashback return is 1.5%:

$24,000 × 1.5% = $360 cashback per year

If you use a higher category cashback card and average 5%, after caps and conditions:

$24,000 × 5% = $1,200 cashback per year

But this assumes your spending fits the card categories and you do not exceed the cashback cap.

Miles scenario

If your card earns 1.2 miles per dollar:

$24,000 × 1.2 mpd = 28,800 miles per year

If you use specialised cards and average 4 miles per dollar on eligible spending:

$24,000 × 4 mpd = 96,000 miles per year

Now the value depends on redemption.

If you value each mile at 1 cent:

96,000 miles = about $960 value

If you value each mile at 2 cents:

96,000 miles = about $1,920 value

That is why miles can look more powerful than cashback.

But again, this only works if you redeem well.

The 2026 Rule of Thumb

Here is the simplest way to decide:

Choose cashback if you want easy, predictable savings.

Choose miles if you want higher travel value.

The Hidden Problem With Cashback Cards

Cashback looks simple, but many cards are not as simple as they seem.

The Hidden Problem With Miles Cards

Miles are powerful, but the learning curve is real.

Can You Use Both Cashback and Miles?

Yes and honestly, this is probably the smartest answer for many people.

A simple hybrid strategy could look like this:

While you usually cannot earn both cashback and miles from the same credit card on one purchase, you may be able to stack separate platform cashback or loyalty rewards with your card rewards on eligible online purchases. That means the real winner may not be cashback or miles. The winner may be stacking rewards properly.

So, Which Gives More Value in 2026?

The honest answer: Miles usually give more maximum value. Cashback gives more reliable value.

If you redeem miles for premium travel, miles can beat cashback.

If you mostly want savings on groceries, dining, shopping, transport, and bills, cashback is usually easier and more practical.

Here is the clearest way to decide:

Final Takeaway

Cashback is like getting a discount on your life. Miles are like building a travel fund with extra steps. In 2026, the better option is not the one with the flashiest advertised rate. It is the one that fits your actual behaviour. If you want simplicity, go with cashback. If you want travel upside and are willing to learn the game, go miles. If you are somewhere in between, use cashback for daily essentials and miles for travel-related or high-earning categories. Because the best credit card strategy is not the one that sounds the most impressive. It is the one you can actually use properly.

Use our credit card comparison tool to have a better idea of which would work better for you!

Shaun

Founder

RealisedGains is committed to empowering retail investors to achieve lasting financial well-being. By delivering meticulously curated investment insights and educational programs, RealisedGains equips individuals with the knowledge and tools to make sophisticated, informed financial decisions.

Founder, Analyst

With over a decade of expertise spanning investment advisory, investment banking analysis, oil trading, and financial advisory roles, RealisedGains is committed to empowering retail investors to achieve lasting financial well-being. By delivering meticulously curated investment insights and educational programs, RealisedGains equips individuals with the knowledge and tools to make sophisticated, informed financial decisions.

Cashback vs Miles: Which One Gives More Value in 2026?

© 2026 RealisedGains | All Rights Reserved | www.realisedgains.com

The go to platform that keeps you informed on the financial markets. Best of all, it's free.

The go-to platform that keeps you informed on the financial markets.

© 2026 RealisedGains | All Rights Reserved | www.realisedgains.com