How Much Do You Need to Buy a HDB as a Single at Age 35?

For many Singaporeans, turning 35 comes with one big financial milestone: finally being eligible to buy an HDB flat as a single. But the real question is not just, “Can I buy?”

It is: “How much do I actually need before I can buy without stressing myself out?”

The answer depends on whether you are buying a 2-room Flexi BTO or a resale HDB flat, how much CPF Ordinary Account savings you have, whether you qualify for grants, and whether you take a HDB loan or bank loan.

Under current HDB rules, Singapore Citizen singles aged 35 and above may buy a flat alone or with up to three other singles. Singles can apply for new 2-room Flexi flats, and CPF notes that singles can now apply for 2-room Flexi flats across all BTO projects under the new classification framework from October 2024.

First, What Can Singles Buy?

As a single buyer aged 35 and above, your main choices are:

Option

What it means

Best for

2-room Flexi BTO

New HDB flat, usually cheaper, but longer waiting time

Singles who want affordability

Resale HDB

Buy from the open market, more expensive, but faster move-in

Singles who want location, space, or speed

A resale flat usually gives you more flexibility in size and location, while a BTO is usually more affordable but requires waiting. Ohmyhome notes that resale flats offer wider location choice, established neighbourhoods, and faster move-in compared with BTO flats.

The 4 Big Costs You Need to Prepare For

When people think of buying an HDB, they usually focus only on the purchase price. But your real budget needs to include:

Downpayment

Cash deposit

Buyer’s Stamp Duty and legal fees

Renovation, furniture, and emergency buffer

This is where many first-time buyers underestimate the real amount needed.

Cost 1: Downpayment

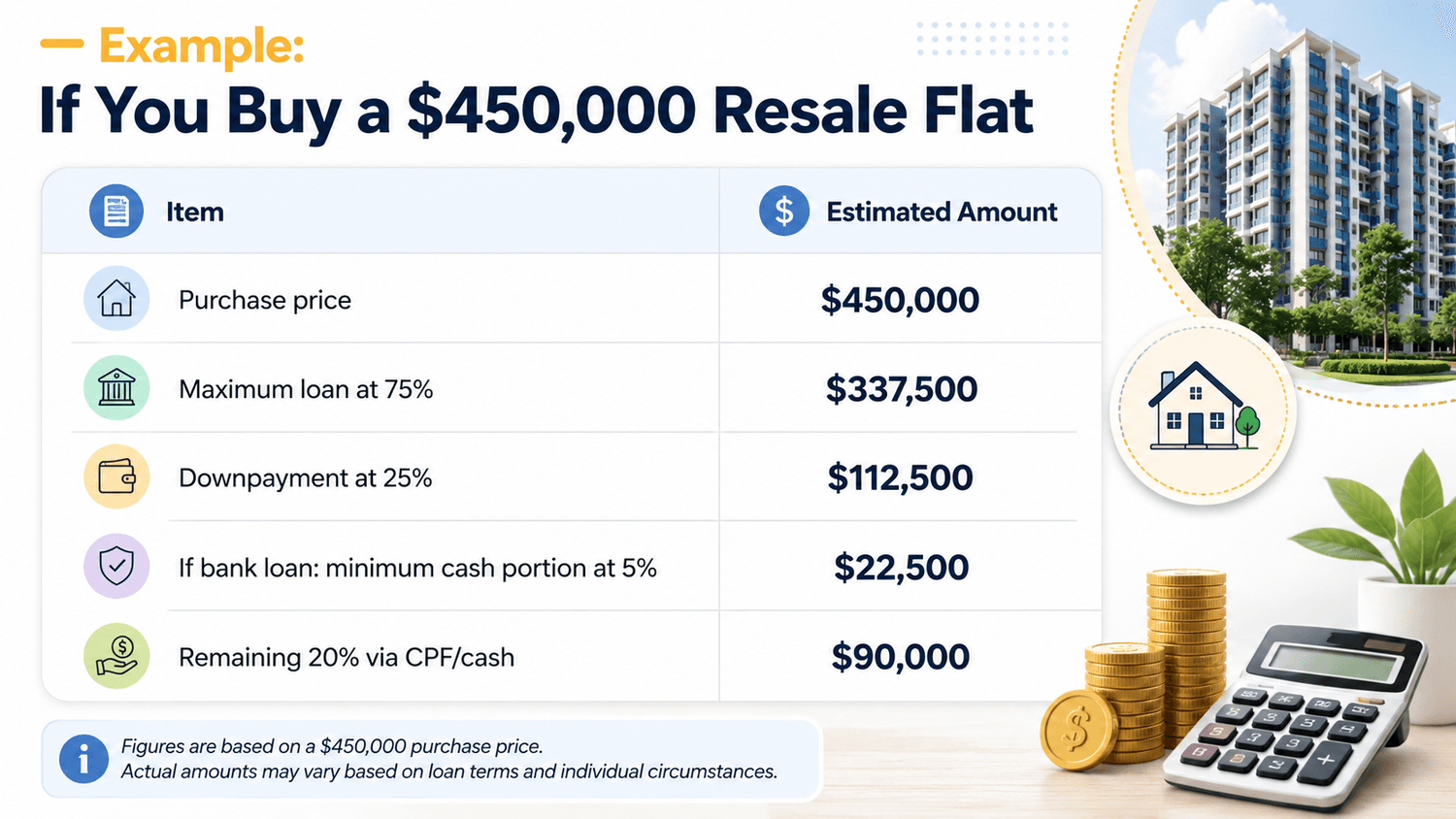

For an HDB housing loan, CPF states that the down payment must be at least 25% of the purchase price, and it can be paid using CPF OA, cash, or both. The maximum HDB loan amount is up to 75% of the purchase price for new flats, and up to 75% of the lower of the resale price or the market valuation for resale flats

.

For a bank loan, CPF states that the down payment is 25%, with at least 5% paid in cash, and the remaining 20% can be paid using CPF OA or cash.

This does not mean you need $112,500 in cash. If you have enough CPF OA, a large part of the down payment can come from CPF. But if your CPF OA is low, your cash requirement goes up.

Cost 2: Cash Deposit to Seller

For resale flats, you need to prepare cash for the Option to Purchase process.

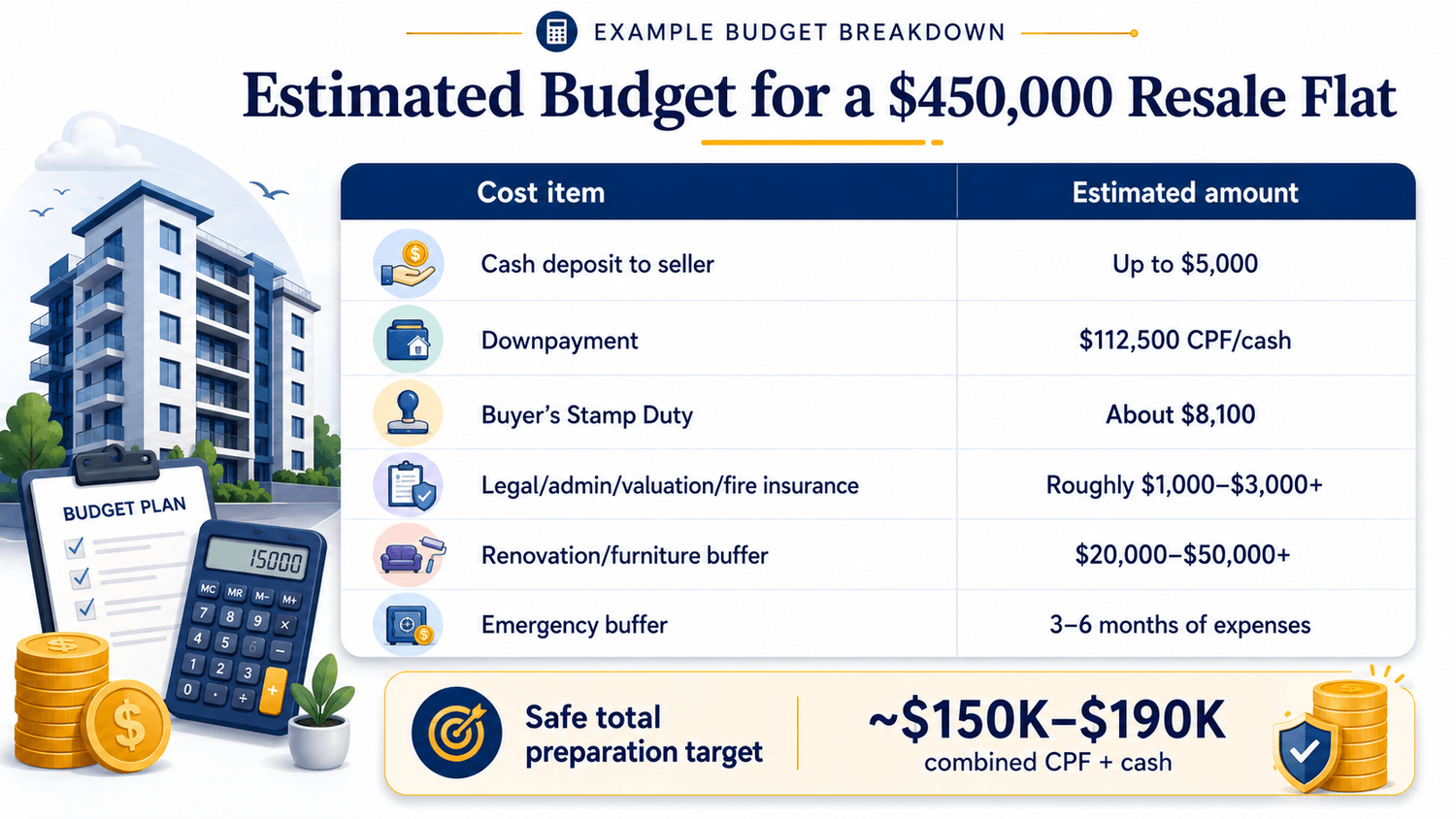

HDB states that the seller grants the Option to Purchase after both buyer and seller agree on the resale price, and the OTP is valid for 21 calendar days. Ohmyhome’s resale guide breaks down the resale deposit as up to $5,000 total, usually made up of an Option Fee of up to $1,000 and an exercise deposit of up to $4,000. So even if you plan to use CPF for most of the purchase, you should still set aside up to $5,000 in cash for the resale deposit

Cost 3: Stamp Duty, Legal Fees, and Admin Costs

In addition to the down payment, you need to budget for transaction costs.

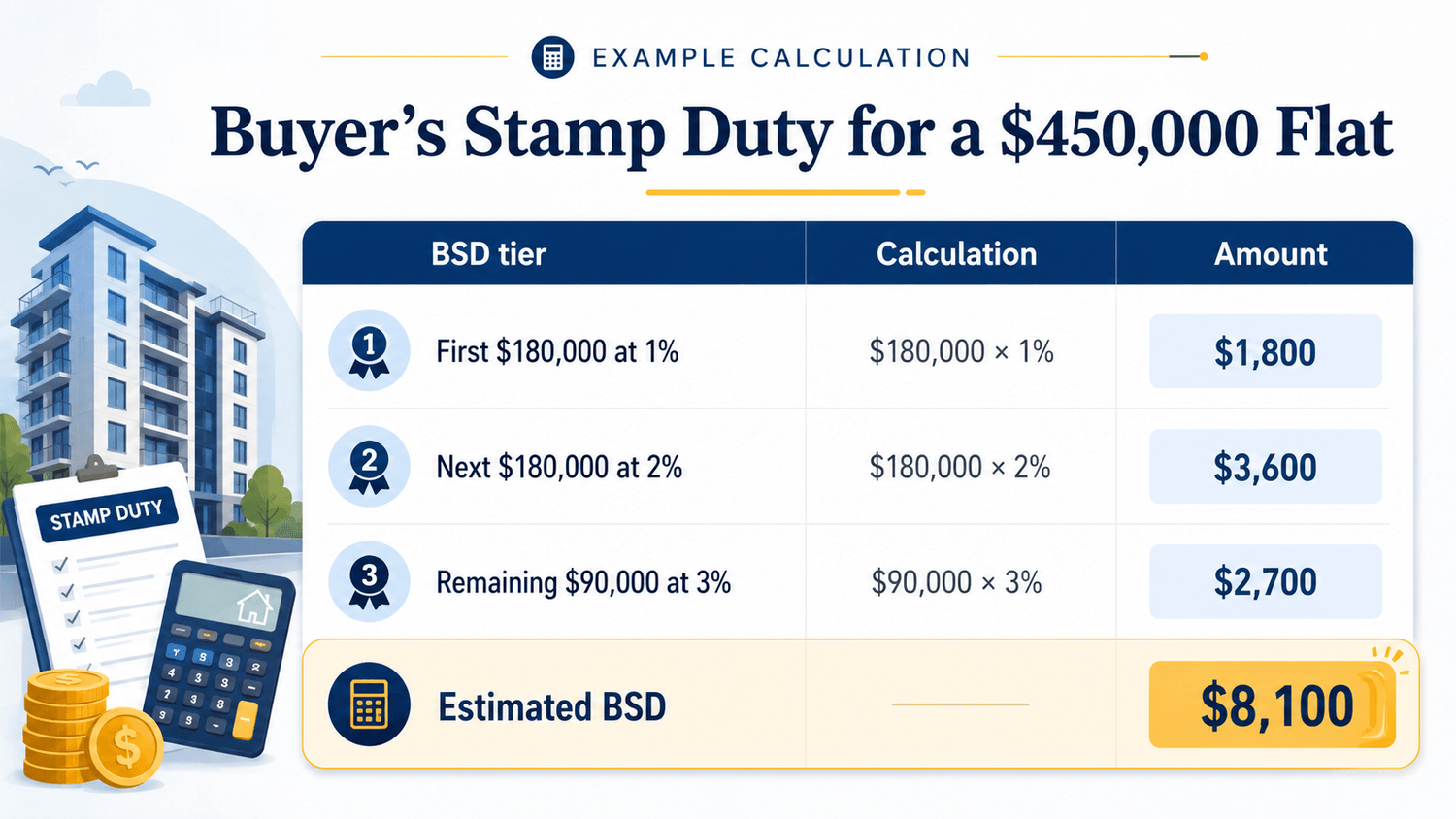

Ohmyhome lists common resale purchase costs, including resale application fees, Buyer’s Stamp Duty, Request for Value fee, fire insurance, Home Protection Scheme, and legal fees. Their guide states resale application fees are $40 for 1- and 2-room flats and $80 for 3-room and larger flats, while Buyer’s Stamp Duty is calculated progressively based on the purchase price.

So for a $450,000 resale HDB, you should budget around $8,000+ for stamp duty alone, before legal and admin fees.

Cost 4: Renovation, Furniture, and Emergency Buffer

This is the part many people forget. Buying the flat is only step one. Moving in costs money, too. For a resale flat, renovation can vary massively depending on the condition. A move-in-ready flat may only need minor work, while an older flat may need work on the flooring, electrical, plumbing, carpentry, painting, appliances, and furniture.

Renovation style

Estimated budget

Minimal touch-up

$10,000–$20,000

Basic renovation

$25,000–$45,000

Heavier resale renovation

$50,000+

CPF also cautions that resale flats can involve more costs than BTO flats, especially because older flats may require more extensive renovation.

Do not spend every dollar on the down payment. You still need cash to actually live in the flat.

So, How Much Should a Single Buyer Prepare?

Here is a simplified example using a $450,000 resale flat.

For a $450,000 resale flat, a single buyer may want to have access to around:

$120,000–$130,000 in CPF/cash for the purchase itself, plus

$25,000–$60,000 in cash/renovation buffer, depending on flat condition.

That means your “safe” total preparation number may be closer to:

$150,000–$190,000 combined CPF + cash. But if you qualify for grants, your required amount may be lower.

What Grants Can Singles Get?

Eligible first-timer singles may receive CPF housing grants. HDB’s singles page links eligible singles to the Enhanced CPF Housing Grant, CPF Housing Grant, and Proximity Housing Grant.

Grant

What to know

Enhanced CPF Housing Grant Singles

Income-based; HDB states the average gross monthly household income must not exceed $4,500 for singles buying a flat.

CPF Housing Grant for Singles Resale

HDB states the income ceiling is $7,000 if purchasing alone.

HDB states the income ceiling is $7,000 if purchasing alone.

HDB states singles may receive $10,000 to live near parents or a child within 4km

HDB has also stated that eligible first-timer singles buying a resale flat can receive up to $115,000 in housing grants.

Important: grants are not “free cash in your bank account.” They are CPF grants credited and used to offset the flat purchase.

BTO vs Resale: Which Is More Realistic?

Choose BTO if:

You want the most affordable route, do not need to move urgently, and are comfortable with a smaller 2-room Flexi flat.

Choose resale if:

You want more space, a specific location, faster move-in, or the option to buy a bigger flat. HDB’s resale statistics page lets buyers view median resale prices by town and flat type, and the resale price index tracks overall price movement in the public housing market. In Q1 2026, HDB reported that the Resale Price Index was 203.4, a 0.1% decrease from Q4 2025. That means resale prices are not something to guess. A single buyer should check actual transaction prices before deciding what they can afford.

Final Takeaway

So, how much do you need to buy an HDB as a single at 35?

The honest answer is:

You do not just need a down payment. You need a full home-buying buffer.

For a resale flat around $450,000, a realistic preparation target could be around $150,000–$190,000 in combined CPF and cash, depending on grants, loan type, renovation needs, and how much CPF OA you already have. For a 2-room Flexi BTO, the amount needed may be much lower, especially if you qualify for grants, but you trade off space and waiting time. The smartest move is to apply for your HDB Flat Eligibility letter, check your CPF OA, estimate your grant eligibility, and work backwards from the monthly mortgage you can comfortably afford. Because buying a home is not just about being eligible. It is about making sure your home does not make you broke.

Shaun

Founder

RealisedGains is committed to empowering retail investors to achieve lasting financial well-being. By delivering meticulously curated investment insights and educational programs, RealisedGains equips individuals with the knowledge and tools to make sophisticated, informed financial decisions.

Founder, Analyst

With over a decade of expertise spanning investment advisory, investment banking analysis, oil trading, and financial advisory roles, RealisedGains is committed to empowering retail investors to achieve lasting financial well-being. By delivering meticulously curated investment insights and educational programs, RealisedGains equips individuals with the knowledge and tools to make sophisticated, informed financial decisions.

How Much Do You Need to Buy a HDB as a Single at Age 35?

© 2026 RealisedGains | All Rights Reserved | www.realisedgains.com

The go to platform that keeps you informed on the financial markets. Best of all, it's free.

The go-to platform that keeps you informed on the financial markets.

© 2026 RealisedGains | All Rights Reserved | www.realisedgains.com